Diversified portfolios surge in Q2, led by a powerful stock market rally A Quarter Notes market update by Terrence Demorest, Chief Investment Officer for Public Markets & ESG and Sam Pecka, Sr. Research Analyst

by Terrence Demorest, Chief Investment Officer for Public Markets & ESG and Sam Pecka, Sr. Research Analyst

The second quarter of 2026 delivered a broad-based rebound in asset prices following a poor start to the year. The backdrop entering Q2 was uncertain, with ongoing conflicts in the Middle East and Ukraine contributing to elevated oil prices and renewed concerns around persistent inflation and the stability of global markets.

Public equities shrugged off those concerns, looking through the noise to find relatively stable economic data. Favorable early-quarter earnings reports, renewed enthusiasm around AI, and a massive IPO for SpaceX late in the quarter created strong tailwinds for global equities.

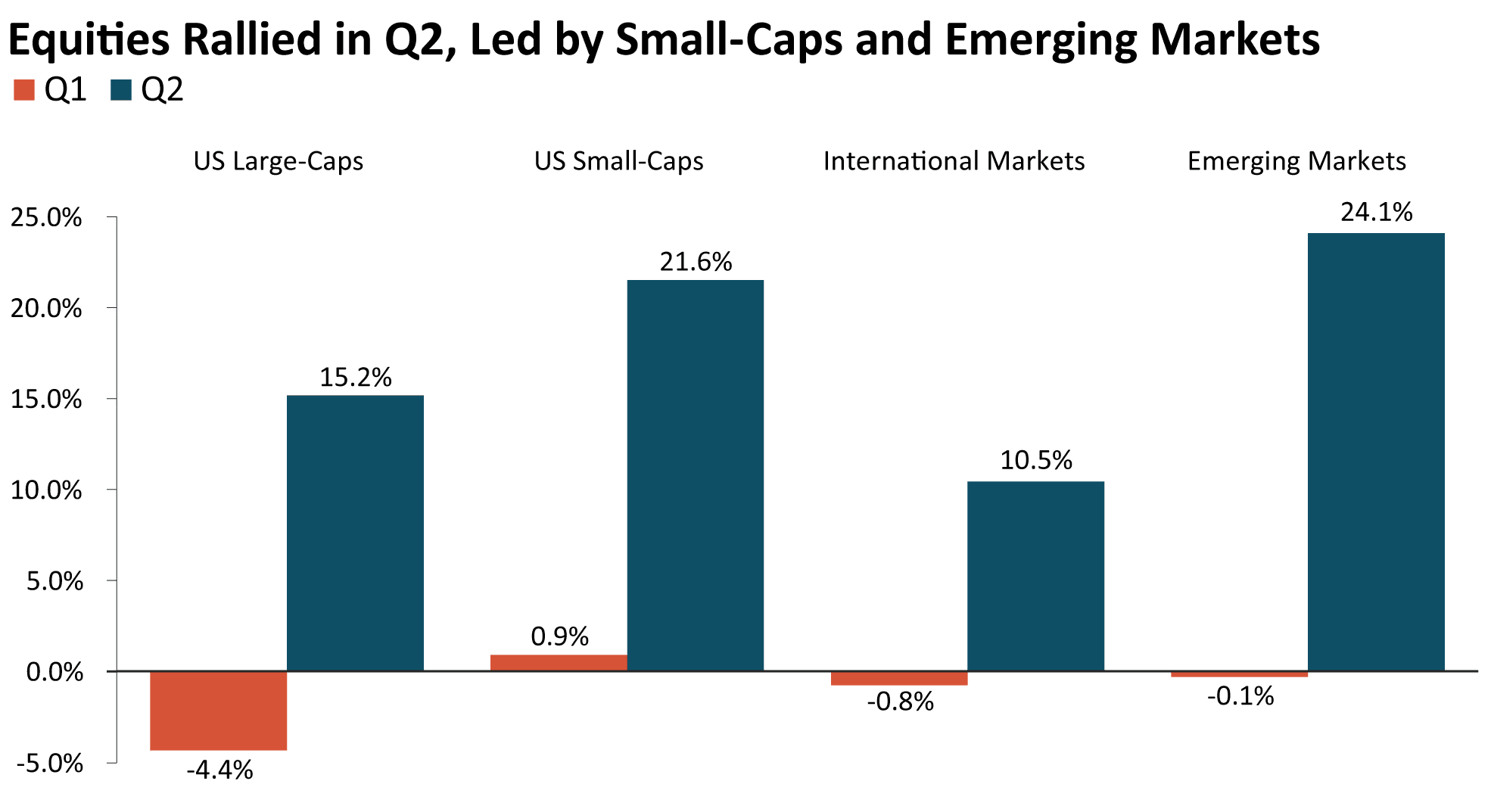

The tech sector, represented by the NASDAQ Composite Index, reversed course sharply and led the rally, rising 21.6% in Q2 with other U.S. indices finishing the quarter not far behind. Foreign equities, most notably those within the MSCI Emerging Markets Index (which is heavily weighted to the information technology sector and specifically to chipmakers), also benefited from the enthusiasm.

By contrast, bond markets continued to search for a clearer signal as yields crept higher during the second quarter. Despite rates remaining unchanged by the Fed in both the April and June meetings, yields have continued to reflect higher inflation expectations and the risk premium bondholders demand for owning longer-term debt.

While the first half of the year has been a tale of two quarters for public equity markets, alternatives have continued to demonstrate the less-correlated nature of their return streams. Observable credit quality remains largely in line with expectations, while overall returns and income yields continue to enhance diversified portfolios.

Private equity also continued to contribute positively to portfolio returns, providing access to the value creation taking place in private markets. Many retail investors are forced to wait on the sidelines until companies go public, but we continue to have conviction in providing access to the value being created in private markets, as well as the diversification these investments can add to a portfolio.

At the time of this writing, tensions in the Middle East have cooled slightly, though the situation remains precarious. A framework for a peace deal has been announced, but negotiations are ongoing and several key issues remain unresolved. Against this backdrop, Brent crude oil prices have fallen to their lowest levels since the conflict first broke out in late February as increasing tanker traffic through the Strait of Hormuz has somewhat eased supply fears.

Looking to the second half of the year, global markets will remain focused on ongoing peace talks. Although oil prices have retreated, several months of elevated prices have pushed inflation to 4.2%, raising the possibility of a rate hike before year-end, a notable reversal from expectations at the start of the year. At the same time, other economic indicators have remained resilient.

As we evaluate these crosscurrents, it is important to reiterate the long-term approach we’ve implemented across our client portfolios. The whiplash from seemingly daily advancements in artificial intelligence, shifting geopolitical tensions, and ever-changing macroeconomic indicators reinforces our conviction in a broadly diversified approach, with an emphasis on mitigating risk while maximizing long-term return potential.

Stocks

As the chart below makes clear, equity markets reversed course and rallied in the second quarter, led by growth-oriented technology companies and small-cap stocks. The Russell 2000, an index tracking smaller publicly traded U.S. companies, posted a near identical 21.6% return for the quarter. This suggests the rally is broadening beyond the largest tech companies and reflects improved confidence in economic growth.

The rally wasn’t unique to U.S. markets; foreign equities also contributed to the turnaround. Most notably, the MSCI Emerging Markets Index posted a 24.1% return after having been down slightly to start the year. International developed equities also posted double-digit returns following a slow start out of the gate for the year.

Two key themes influenced equity markets throughout the second quarter, and we expect both to remain important drivers for the foreseeable future: energy prices and artificial intelligence. The first has shaped market cycles for decades, while the second is a rapidly growing category that has captured investor attention.

Energy prices, which reached their highest levels in roughly four years during Q2, declined sharply during the final month of the quarter as the potential for a peace agreement between the U.S. and Iran appeared to gain traction. For each tanker that safely navigates the Strait of Hormuz, supply concerns ease and the price per barrel of oil moves lower. In turn, investor anxiety around persistent inflation and the direction of interest rates also subsides.

The durability of artificial intelligence valuations, and the spending required to support them, has also been widely discussed throughout the first half of 2026. Concerns that investment could slow, or that demand may be peaking, were largely offset by a steady flow of positive news during Q2. OpenAI announced a favorable equity raise, hyperscalers increased their guidance on capital expenditures (which analysts estimated could top $700 billion in 2026), and Nvidia reported demand that continued to outpace supply. These developments came alongside generally strong earnings reports and the largest IPO in history (SpaceX), further reinforcing investor enthusiasm for next-generation businesses.

Alternatives – Growth

Private equity markets continue to be selective, as liquidity and dealmaking remain challenged. Global buyout value sputtered in the second quarter for many of the reasons discussed above. However, the lack of traditional liquidity options continues to benefit secondary markets, as investors seek liquidity in a more constrained exit environment.

Despite the broader malaise, significant value continues to be created in private markets. Select transactions are still clearing at attractive prices, albeit primarily for top-tier assets. Anthropic and OpenAI both filed S-1s during the second quarter, solidifying their intentions to go public, while SpaceX completed its journey as a private company and transitioned to the public markets in one of the most anticipated and largest IPOs ever. In the process, these events enriched many private market participants and highlighted the value creation that can occur before companies become accessible to public market investors.

Alternatives – Income

Private credit continues to deliver attractive income and a less volatile return pattern than traditional fixed income. This might come as a surprise to casual readers of the financial press, as hyperbolic headlines have brought undue scrutiny to the asset class in the first half of 2026.

Despite the noise, we have not observed material deterioration in the underlying credit quality of the broader asset class. Like any financial market, private credit spans a nuanced spectrum of risk and return opportunities, which we continue to evaluate carefully as we seek to optimize portfolios.

Liquidity is a key consideration when evaluating access to any market. Intuitively, one might assume more liquidity is always better. However, investors are often compensated with an illiquidity premium when they are willing to accept less frequent access to capital. For long-term investors, more limited liquidity, including the use of redemption gates—limits on the amounts that can be redeemed at any particular time—can also help align investment horizons and reduce the need for forced asset sales, ultimately protecting investor returns. While the media continues to frame these situations negatively, the fundamentals in this space remain attractive, and we continue to collect income with a focus on long-term value creation.

Bonds

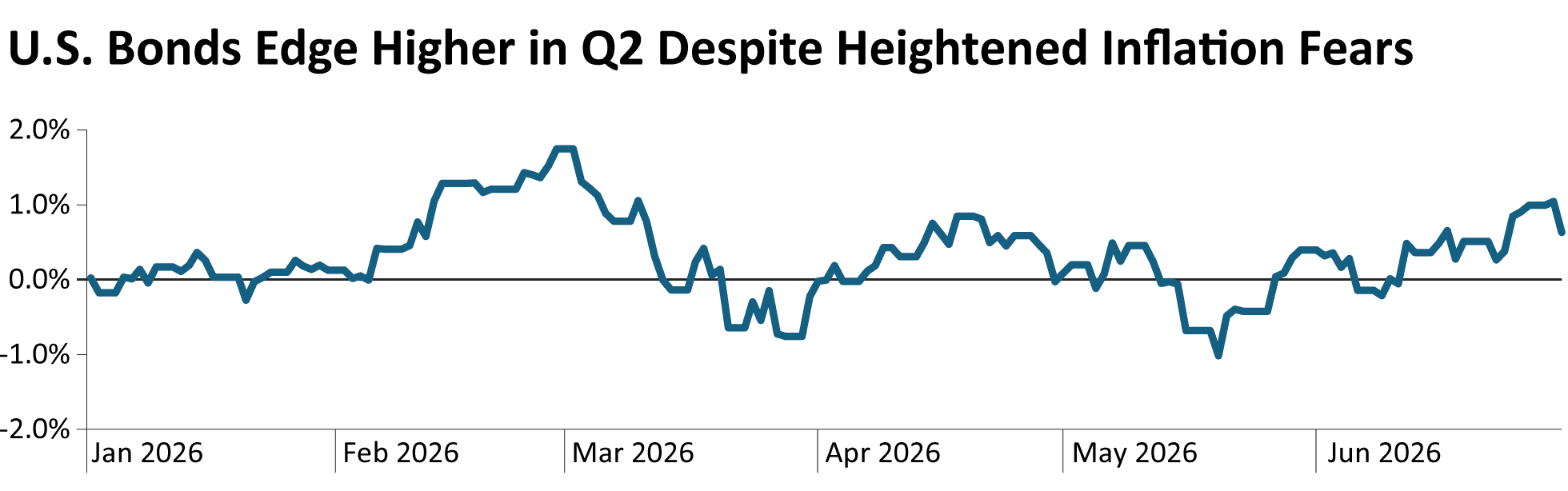

The U.S. bond market, represented by the Bloomberg U.S. Aggregate Bond Index (shown in the chart below), bounced around during the second quarter and ultimately closed out the first half up slightly, 0.6%. Inflation reaccelerated during the quarter, with the CPI rising from 3.3% in March to 4.2% by quarter-end. At the same time, unemployment remained steady at 4.3% and consumer spending continued to signal healthy economic activity, supporting the broader narrative of a resilient economy.

The stronger economic data eased near-term recession fears, reducing the likelihood of Fed rate cuts. Investors also priced in elevated inflation and demanded additional compensation for owning longer-dated Treasuries amid heightened uncertainty, which sent yields higher throughout the interest rate curve.

The second quarter also saw the transition to Kevin Warsh as Fed Chair in May. Although appointed by a president seeking lower interest rates, Warsh has already surprised some by being more hawkish on inflation, favoring a firm policy stance while inflation remains above the Fed’s 2% target. His early comments also emphasized less forward guidance on the Fed’s next moves, leaving markets with less clarity on the path of interest rates. The trade-off between more attractive (lower) yields and persistent inflation will likely be the central question guiding bond market and Fed activity.

During the second quarter, we added a new fund, the CrossingBridge Ultra-Short Duration Fund (CBUDX), to our bond allocation. The addition increased overall credit quality in the portfolio through greater investment-grade (IG) exposure. Given recent uncertainty, we feel the higher IG exposure should exhibit lower volatility if the economy were to deteriorate. We continue to favor shorter and intermediate-maturity bonds, which offer attractive income while limiting exposure to further increases in interest rates. This positioning helps preserve flexibility in an environment where persistent inflation and a more accommodative stance towards rates remain uncertain and in conflict.

Recent posts

Sources

Source for charts: Bloomberg as of June 30, 2026. Indices used: U.S. large-caps: S&P 500; U.S. small-caps: Russell 2000 Index; International equities: MSCI All Country World Index; Emerging markets: MSCI Emerging Markets Index; U.S. Bond Market: Bloomberg U.S. Aggregate Bond Index.

Disclosures

This content was prepared by Westmount Partners, LLC (“Westmount”). Westmount is registered as an investment advisor with the U.S. Securities and Exchange Commission, and such registration does not imply any special skill or training. The information contained in this content was prepared using sources that Westmount believes are reliable, but Westmount does not guarantee its accuracy. The information reflects subjective judgments, assumptions and Westmount’s opinion on the date made and may change without notice. Westmount undertakes no obligation to update this information. It is for information purposes only and should not be used or construed as investment, legal or tax advice, nor as an offer to sell or a solicitation of an offer to buy any security. No part of this content may be copied in any form, by any means, or redistributed, published, circulated or commercially exploited in any manner without Westmount’s prior written consent.

Past performance is not indicative of future results. Investment returns will fluctuate, and investors may experience a loss. No guarantee or representation is made that any investment strategy will be successful or achieve any particular results. All investments involve risk, including the possible loss of principal. Different types of investments involve varying degrees of risk, and there is no assurance that any specific investment will be profitable.

The financial advice and recommendations that we provide are tailored to each client’s unique circumstances. Please remember to contact us if there are any material changes in your financial situation or investment objectives, or if you wish to add or modify any restrictions to your investment portfolios.

If you have any comments or questions about this content, please contact us at info@westmount.com.