Public markets face headwinds while private markets demonstrate resilience A Quarter Notes market update by Terrence Demorest, Chief Investment Officer for Public Markets & ESG

by Terrence Demorest, Chief Investment Officer for Public Markets & ESG

The first quarter of 2026 showed a clear divide between public and private markets, highlighting why diversification and alternative investments can play such an important role in client portfolios.

While public equity markets faced headwinds from geopolitical tensions in the Middle East, private markets continued to demonstrate the stability and resilience that make them an essential component of well-constructed portfolios.

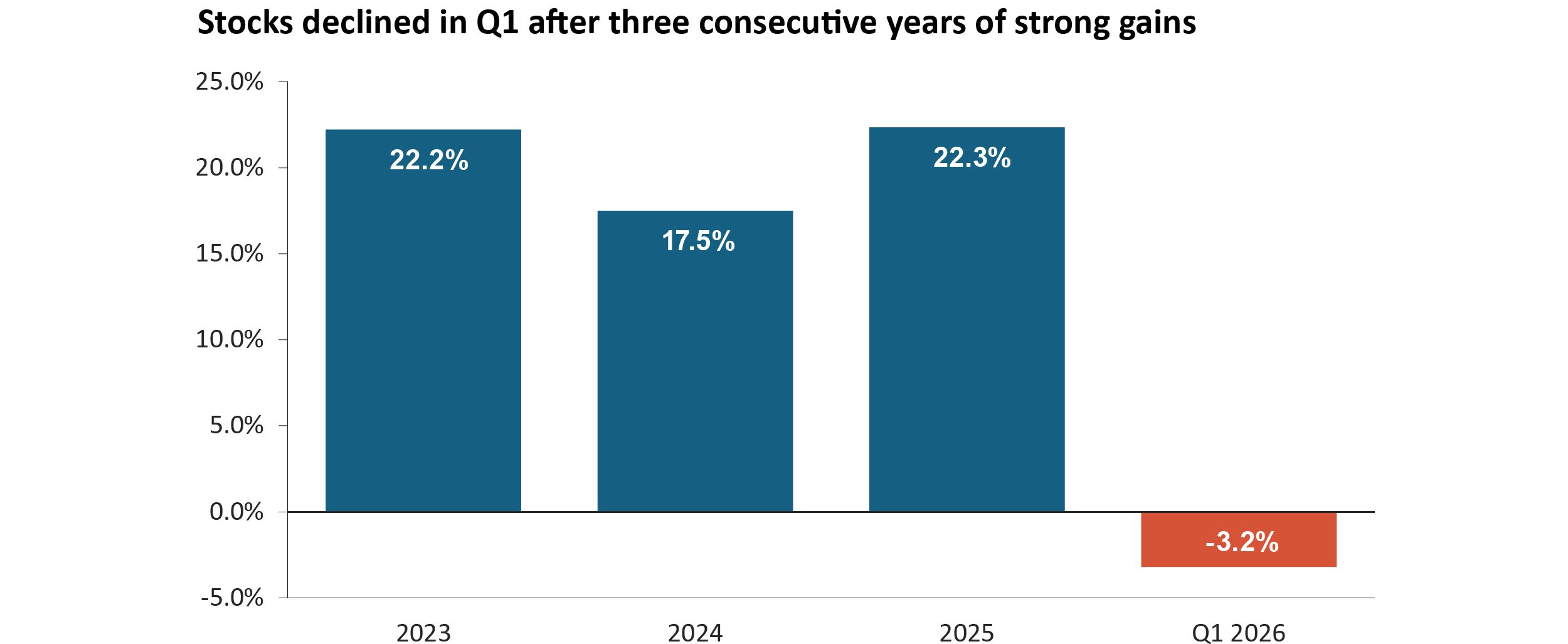

U.S. stocks pulled back during the quarter, with the S&P 500 declining -4.4%, as investors reacted to uncertainty around the conflict in Iran and how it could impair global growth. The global stock market (a mix of U.S. and foreign stocks) declined -3.2% for the quarter, reflecting similar concerns across international markets.

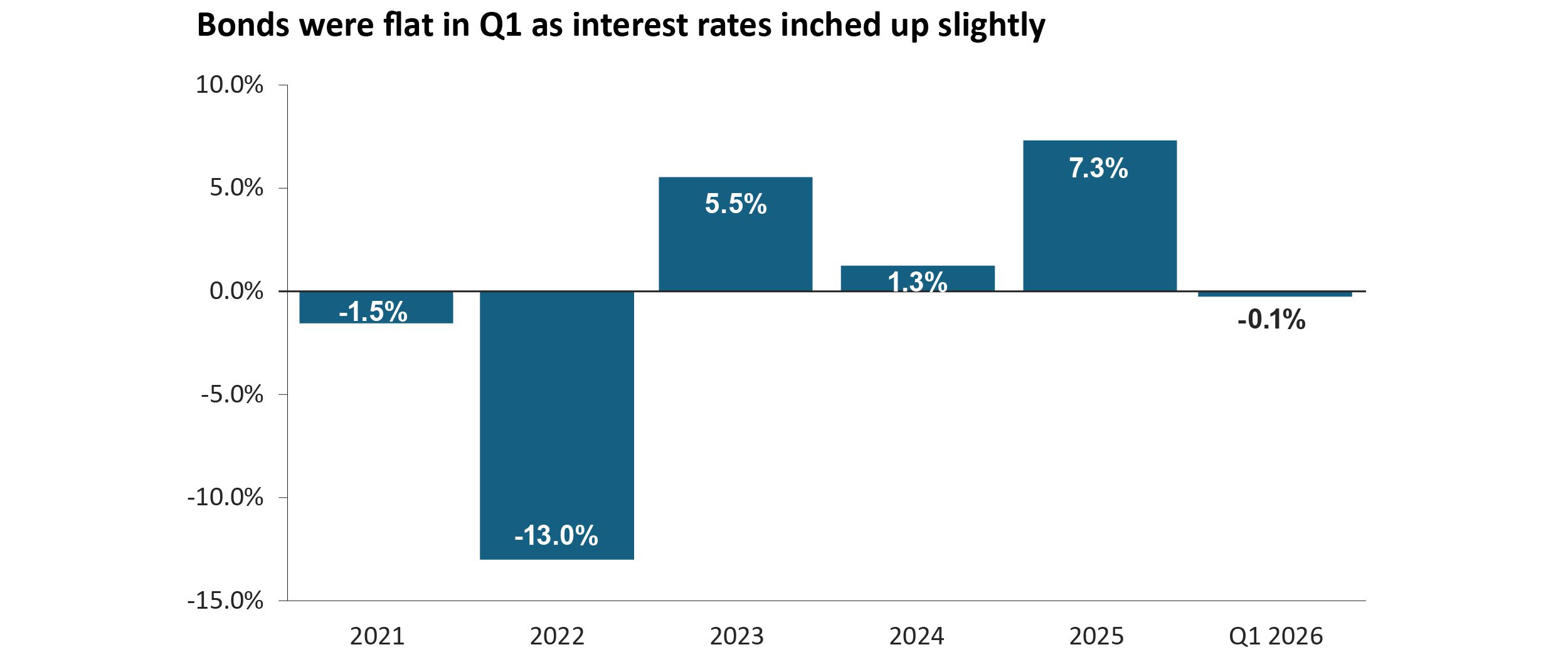

Bonds also faced pressure, down -0.1% for the quarter. Inflation fears related to surging energy prices led to modest selling in fixed-income markets, even as the Federal Reserve held interest rates steady at 3.75% throughout the quarter.

Against this backdrop of public market volatility, alternative investments once again proved their worth. Private credit continued its lengthy track record of consistent performance, delivering positive returns while providing steady income to portfolios.

Private equity maintained its role as a source of long-term growth and diversification, demonstrating again that private markets often move independently of public market sentiment.

The quarter also brought increased media attention to private credit, with some hedge fund managers attempting to profit by stirring up investor concerns. While this caused increased redemption requests at certain funds, the underlying fundamentals in private credit remain sound, returns continue to be positive, and well-managed funds continue to protect existing investors.

This episode reinforces why private markets deserve a place in diversified portfolios: they offer an illiquidity premium that rewards patient investors and remain insulated from the daily noise that can drive public market swings.

Looking ahead, the investment landscape remains uncertain. If tensions in the Middle East ease, the impact on the U.S. economy would be limited and public markets could recover their first quarter losses. The underlying U.S. economy remains healthy, with unemployment at 4.4% and inflation at 2.4%.

A more protracted conflict, or longer-term disruptions in the supply and distribution of oil, though, would likely lead to further stock market declines. Staying balanced across both public and private markets and keeping a long-term mindset is still one of the best ways to navigate uncertainty while aiming for solid long-term returns.

Stocks

The first quarter began on an uncertain note as escalating tensions in the Middle East weighed on investor sentiment. Concerns about the conflict’s impact on global growth, combined with fears of an inflationary shock from disrupted energy supplies, led to broad declines across equity markets. As the chart below shows, the S&P 500 fell -4.4% for the quarter, marking its weakest performance since the third quarter of 2022.

Sector performance told the story of a market driven by geopolitical risk. Energy stocks surged +38.3% as oil prices climbed on supply concerns, while defensive sectors also performed well. Materials gained +9.7% and utilities rose +8.3% as investors sought safety. Industrials added +4.6%, benefiting from infrastructure spending and defense-related demand.

Growth-oriented sectors bore the brunt of the selloff. Communications services fell -6.9%, while financials declined -9.4% on concerns about economic growth. Consumer discretionary stocks dropped -9.2%, as investors worried about the impact of higher energy prices on consumer spending.

International markets fared slightly better than U.S. stocks. Emerging markets declined just -0.1% for the quarter, demonstrating surprising resilience. U.S. small-cap stocks edged up +0.9%, outperforming their large-cap counterparts.

The quarter’s volatility served as a reminder that even after three consecutive years of double-digit gains, equity markets remain vulnerable to unexpected shocks (and inevitably, to both strong and weak economic environments). Corporate earnings, the trajectory of Middle East tensions, and the Federal Reserve’s policy stance will be key drivers of market performance in the near-term.

Alternatives – Growth

Private equity markets continued to function effectively throughout the first quarter, demonstrating the advantage of private market valuations that do not fluctuate with daily headlines. While public market investors reacted to geopolitical concerns by selling stocks, private equity portfolios maintained their focus on long-term value creation.

Deal activity remained healthy despite public market volatility. The private equity holdings in client portfolios, including the Cascade Private Capital Fund and the StepStone Private Equity Strategies Fund, continued to provide access to opportunities across private markets. These strategies benefit from purchasing existing ownership stakes at discounts and participating in co-investment opportunities alongside established managers.

The divergence between public and private market performance in the first quarter highlighted the diversification benefits that private equity brings to portfolios. While public equity investors faced daily price swings driven by news headlines, private equity investments remained focused on operational improvements and strategic growth. We expect private equity to remain an important source of long-term growth and portfolio diversification.

Alternatives – Income

Private credit delivered another quarter of positive returns in early 2026, maintaining its track record of consistent performance even as public markets faced headwinds. The asset class continued to generate reliable income with lower volatility than traditional fixed income.

The first quarter brought unprecedented media attention to private credit, much of it negative and some of it driven by hedge funds seeking to profit from investor anxiety (they do so by shorting the stocks of investment firms specializing in private credit, and in buying existing private loans at more favorable—lower—prices).

Headlines focused on redemption requests at several funds, which created concern among some investors. However, a closer examination reveals a very different picture.

The fundamentals underlying private credit remain sound. Borrowers have continued to service their obligations, default rates remain low, and loans are typically secured by tangible assets including corporate cash flows and real estate. Returns across private credit strategies have remained positive, and redemption requests have been managed responsibly.

Well-managed funds have protected existing investors by utilizing gates and other liquidity management tools exactly as designed. Some funds have met redemption requests in full or have had sponsor support to do so, demonstrating the strength of their portfolios.

Most importantly, the redemptions have had zero impact on the underlying fundamentals of private credit portfolios. The asset class continues to perform as expected, generating attractive risk-adjusted returns.

This episode reinforces why private credit deserves a place in diversified portfolios. The illiquidity premium exists precisely because private credit does not offer daily liquidity. Investors who understand this and maintain a long-term perspective have been rewarded with higher yields and more stable returns than traditional bonds can offer.

For considerable time now, private credit managers have stepped in to fill the gap created when banks pulled back from middle-market lending. Higher yields, strong fundamentals, positive returns, and lower correlation to public markets have made private credit an increasingly compelling alternative to traditional bonds.

Bonds

The U.S. bond market faced modest headwinds in the first quarter, declining -0.1%. The decline reflects investor concerns about potential inflation pressures from surging energy prices related to the Middle East conflict, as shown in the chart below:

The Federal Reserve held interest rates steady throughout the quarter, maintaining the federal funds rate at 3.75%. Policymakers signaled a cautious approach, noting that while inflation has moderated to 2.4%, it remains above the Fed’s 2% target. The labor market showed continued health, with unemployment at 4.4%, giving the Fed room to remain patient before implementing additional rate cuts.

Bond investors found themselves caught between competing forces. Yields remain attractive as a source of income, but inflation concerns related to energy prices limited the potential for bond price appreciation during the quarter. The slight decline stood in contrast to the strong +7.3% gain bonds delivered in 2025.

Looking ahead, the outlook for bonds will depend heavily on the trajectory of inflation and the Fed’s response. If energy prices stabilize as Middle East tensions ease, inflation pressures should lessen, potentially allowing the Fed to resume rate cuts later in 2026.

This environment reinforces our continued emphasis on shorter maturity bonds and alternative income strategies, particularly private credit, which can offer higher yields with less sensitivity to interest rate movements than traditional fixed income. The first quarter served as a reminder that diversification across income generating assets, both public and private, remains essential for managing risk while pursuing attractive returns.

Recent posts

Qualified small business stock

Discover a powerful yet overlooked tax provision for business owners navigating a sale

Sources

Source for “Stock market” chart: Bloomberg as of April 1, 2026. Indices used: Stock Market: MSCI All Country World Index; Bond Market: Bloomberg U.S. Aggregate Bond Index.

Disclosures

This content was prepared by Westmount Partners, LLC (“Westmount”). Westmount is registered as an investment advisor with the U.S. Securities and Exchange Commission, and such registration does not imply any special skill or training. The information contained in this content was prepared using sources that Westmount believes are reliable, but Westmount does not guarantee its accuracy. The information reflects subjective judgments, assumptions and Westmount’s opinion on the date made and may change without notice. Westmount undertakes no obligation to update this information. It is for information purposes only and should not be used or construed as investment, legal or tax advice, nor as an offer to sell or a solicitation of an offer to buy any security. No part of this content may be copied in any form, by any means, or redistributed, published, circulated or commercially exploited in any manner without Westmount’s prior written consent.

Past performance is not indicative of future results. Investment returns will fluctuate, and investors may experience a loss. No guarantee or representation is made that any investment strategy will be successful or achieve any particular results. All investments involve risk, including the possible loss of principal. Different types of investments involve varying degrees of risk, and there is no assurance that any specific investment will be profitable.

The financial advice and recommendations that we provide are tailored to each client’s unique circumstances. Please remember to contact us if there are any material changes in your financial situation or investment objectives, or if you wish to add or modify any restrictions to your investment portfolios.

If you have any comments or questions about this content, please contact us at info@westmount.com.